The Scene

One thing stood out at Semafor’s second annual Business Summit in New York on Monday: the perils of the mushy middle.

There were fascinating and newsy conversations in their own right — Pfizer CEO Albert Bourla on Covid lessons, National Women’s Soccer League Commissioner Jessica Berman on Caitlin Clark, Advent’s John Maldonado’s respectful advice to Elizabeth Warren.

But the business world has always been a dynamic barbell: Companies grow, turn into hulking behemoths, and throw off talent and ideas and capital that seed smaller upstarts. It’s the corporate carbon cycle and it works well. But it’s spinning faster these days, and that middle ground — undifferentiated, undercapitalized, and without the benefits of either speed or scale — is increasingly deadly.

Maldonado and JAB’s Anant Bhalla talked about it in the investing world, where financial superstores are zooming away from specialists. Jon Pruzan, formerly of Morgan Stanley and now at Pretium, talked about it for banks, a year after the regional lending crisis. Berman talked about it in sports: “We have the sophisticated investors and capital and support from media partners and sponsors to ensure that we can compete with the Big Four in the men’s leagues” and not get stuck competing for eyeballs with pickleball and professional slap-fighting. Read below for highlights from the event.

Semafor Business Summit

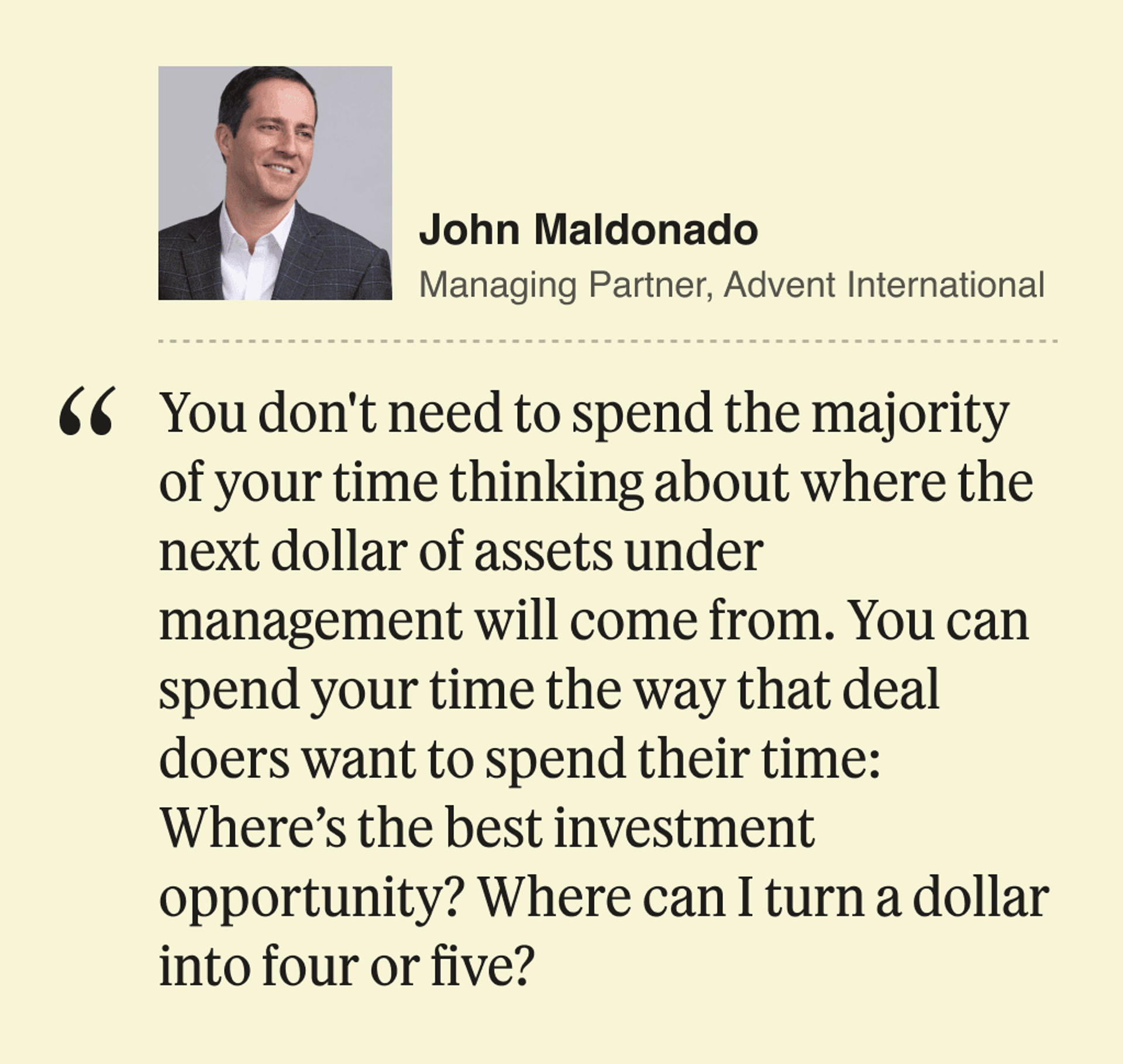

The private-equity industry is splitting. Publicly traded firms like Blackstone ($1 trillion in assets) and KKR ($580 billion) are turning into financial supermarkets, leaving firms like Advent, with about $90 billion, facing a choice to try to beat them — by focusing on returns in their core businesses of corporate LBOs — or join them. Maldonado says Advent is betting on the former and has no plans to go public. Seeing my skepticism, he added a caveat: “If the tectonic plates shifted in a way where all of a sudden we can’t do the things we need to do to be great investors, we will revisit that assumption.”

We also touched on healthcare investing, Maldonado’s specialty and the target of increasing scrutiny from Washington after a string of bankruptcies and bad patient outcomes: “If Elizabeth Warren were here, I might suggest there’s a lot of great ideas, not to mention capital and insight and innovation, that can come from the private sector.”

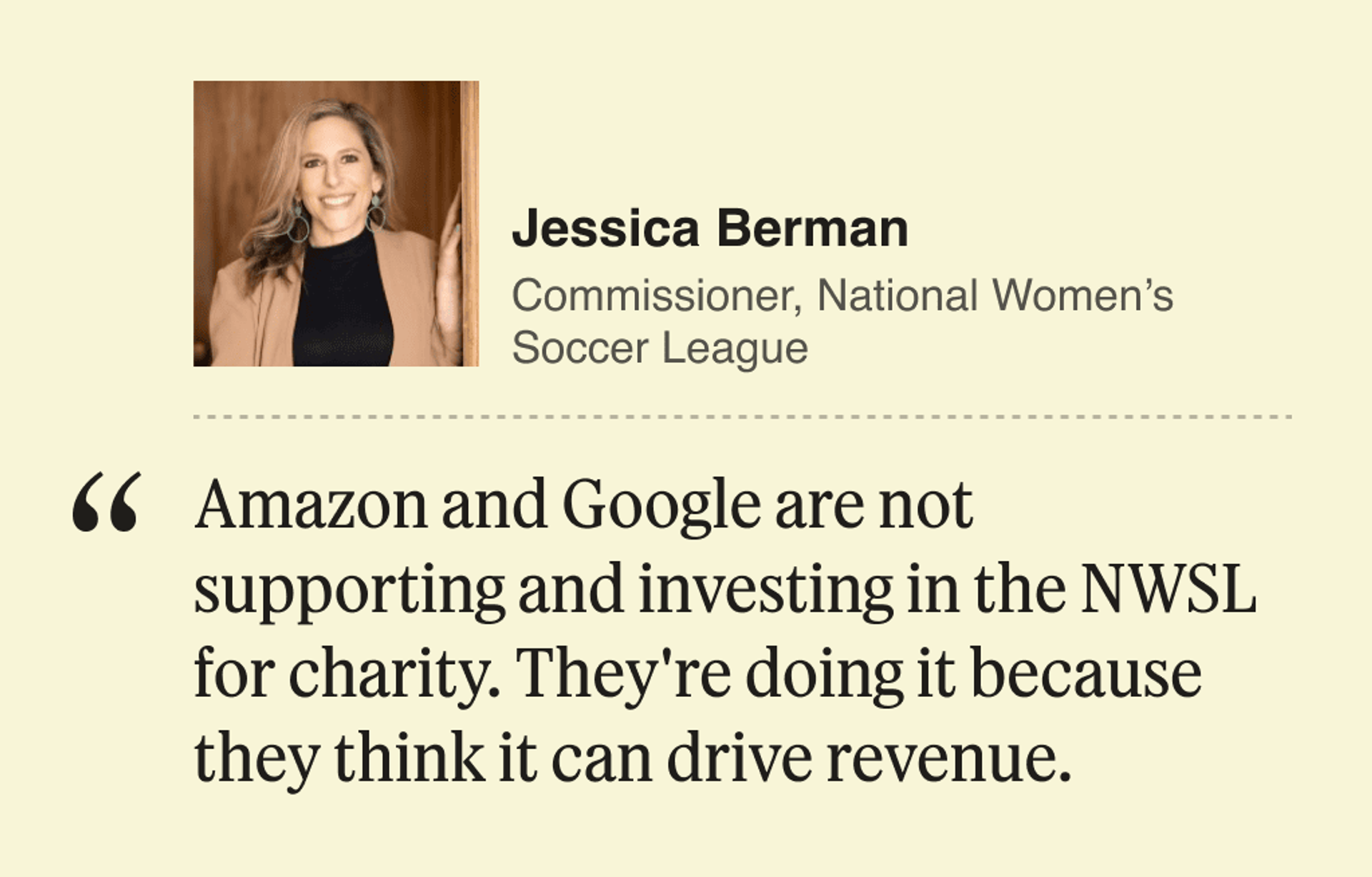

Berman was in Cannes last week, selling corporate sponsors on women’s soccer, which has historically been more of a DEI consideration than an ROI one. She says that’s starting to change, helped in large part by a blockbuster media-rights deal the league signed last year — $240 million, across streaming (Amazon) and linear TV (CBS, ESPN, and ION).

The league’s choice to go with Amazon is itself a compelling datapoint for the Everything Store’s ambitions in content: “As long as you have a Prime Video membership, which is virtually everybody in our country, you can see our games,” she said, “so we get the streaming audience without burying it behind a paywall.”

We talked about the influx of Wall Street money into sports in general and NWSL in particular, which was the first major sports league to allow institutional investors to control teams. “We have to be very cautious and careful [but] I’m obviously a fan of it,” she said, singling out Sixth Street, which owns San Francisco’s Bay FC through its evergreen fund. A sports team “is not something that you hold for five years and expect to make money,” she said, “and that requires a different kind of investor.”

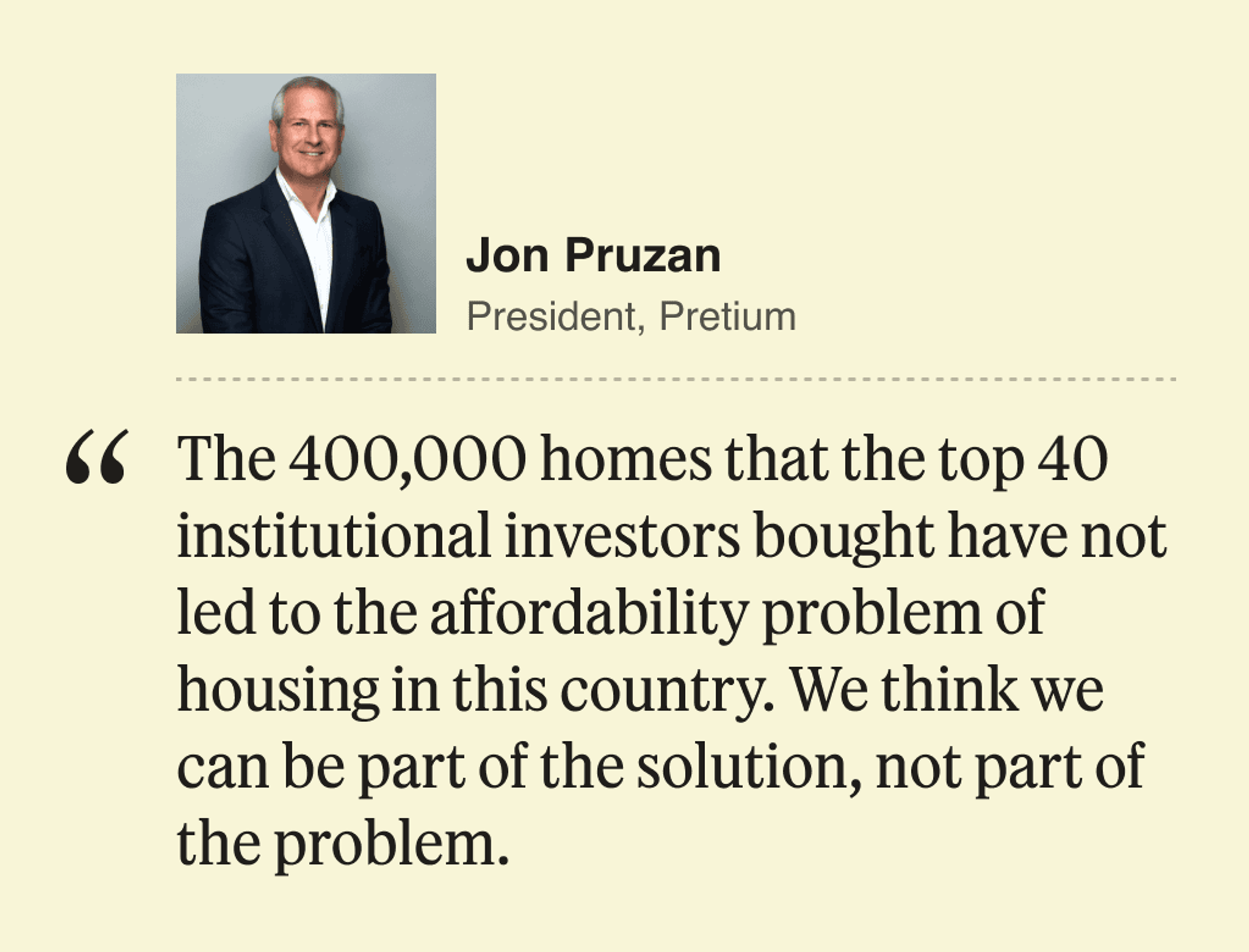

Pruzan, who retired as one of Morgan Stanley’s top executives last year, hit back at the narrative that firms like Pretium are contributing to the housing crunch. He noted that Wall Street firms aren’t squeezing out buyers — home ownership rates have been pretty steady historically in the mid-60% range — but rather smaller landlords who can’t offer 24/7 maintenance. “We as an industry are doing better than the traditional mom and pop who own two or three units,” he said.

We also talked about his old life in banking, where midsized firms face fleeing deposits, growing compliance costs, and shrinking loan books. “Since I retired, nothing good has happened for bank profitability.” He likes a “Canada on steroids” model, with a few dozen big banks on one end and small community lenders on the other. “All these banks in the middle are going to come under immense pressure because they’re competing against people that have $2 trillion, $3 trillion balance sheets,” he said. “It gets harder and harder.” (For more on that, read my recent interview with PNC’s chief executive Bill Demchak, who is trying desperately to get out of that uncomfortable middle.)

I’ve spent the past nine months watching people’s eyes glaze over when I tell them that insurance is the most interesting corner of finance, so I was delighted to sit down with Bhalla. He built American Equity Life into a major insurer and sold it last year to private-equity firm Brookfield, and is now rebuilding inside JAB, the investment arm of the Reckitt Benckiser family.

He was an incredibly good sport when I suggested, more than once, that this was all going to end terribly for policyholders, and he acknowledged the risk of bad actors giving in to bad incentives. “If you wake up as an asset manager and say ‘Gosh, I wish I had insurance funding because I could now fund my [deals] with long-term money at 4%,’ that’s not the right motivation structure,” he said. “Because you’re thinking ‘how do I find more and more assets? How do I make more and more in fees?’”

“Fee-related earnings are a drug,” he said in the evening’s pull-quote for a particular kind of Wall Street nerd (hi, it’s me.)

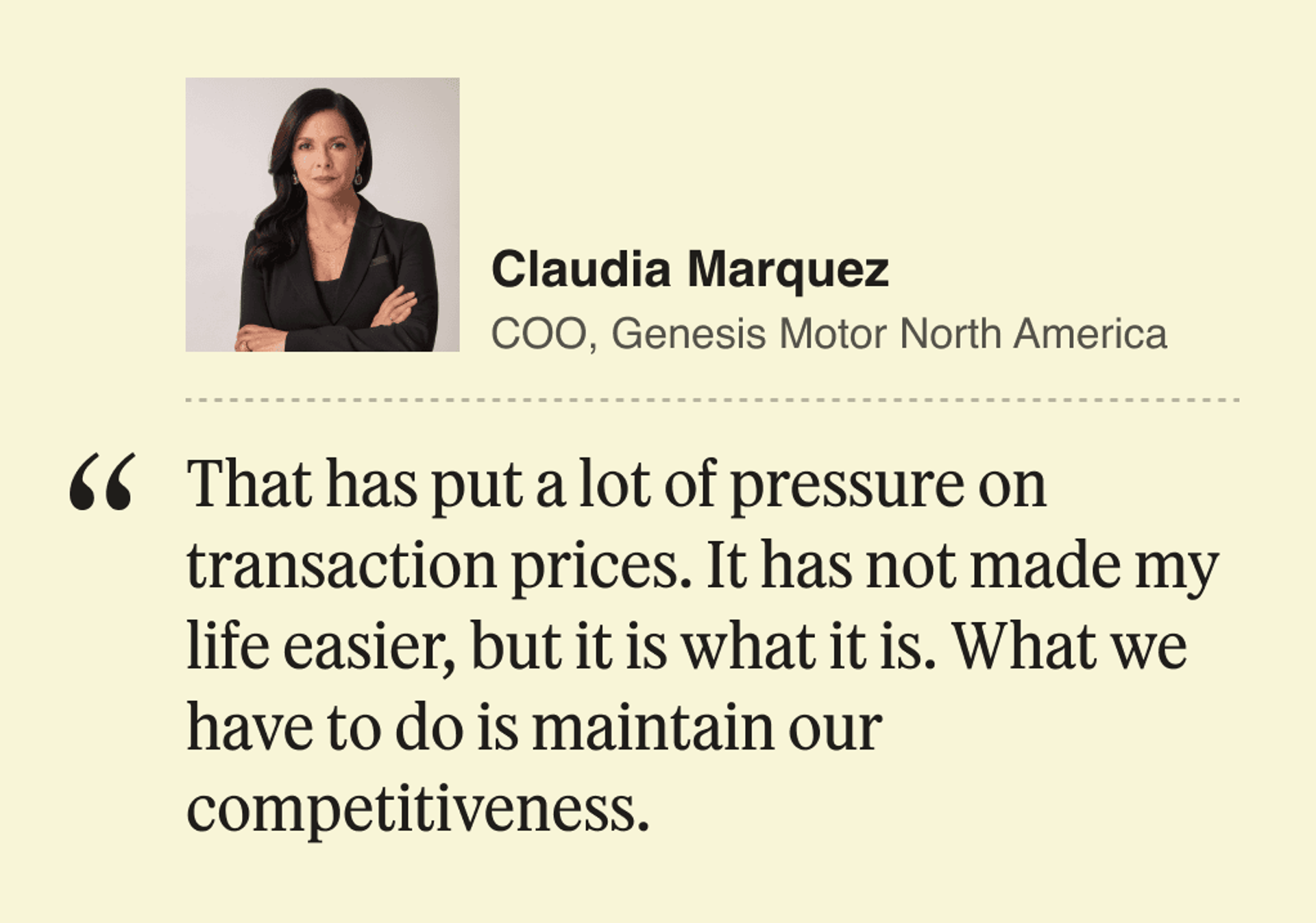

That was Marquez, who has spent three decades working for automotive brands including BMW and Infiniti and, now, Hyundai’s luxury brand, Genesis, on the effects of inflation and higher interest rates on luxury buyers.

Still Genesis has made inroads in the US, where sales are strongest in south Florida — no surprise to anyone who has followed Wall Street’s coastal exodus. Like other carmakers, it is betting heavily on electric vehicles but wary of consumer demand that has proven to be fickle. In May, 18% of Genesis’ sales were EVs, double 2023’s annual figure, she said, and the company struck a deal last year to gain access to Tesla’s network of charging stations. “We have to always think [about] what we need to do for adoption, and for consumers to have less anxiety,” she said.

Pfizer, as far as can be said about any company, had a great pandemic. Its post-pandemic run has been tough. The stock is down by more than half from its 2021 high, and Bourla has made an all-in bet on cancer. He readily acknowledged the company’s miscalculations about demand for vaccines and about the science-skepticism that turned one of the great pharmaceutical wins in history into a PR minefield and that’s still hanging around today’s politics.

“We stayed with the manufacturing and laboratory infrastructure that was there to support a way bigger business,” he said. “Covid is not what it used to be.” Cue a $4 billion cost-cutting effort.

We also talked about the weight-loss craze, where Pfizer is working on a competitor to Ozempic and Wegovy, which have done wonders for Novo Nordisk’s and Eli Lilly’s share price. He suggested Wall Street is a bit overenthusiastic: “Right now it is almost a duopoly, so it’s very lucrative,” he said “But there are dozens of companies that are preparing competing products, so when all of this hits the market, probably the price will go down.”