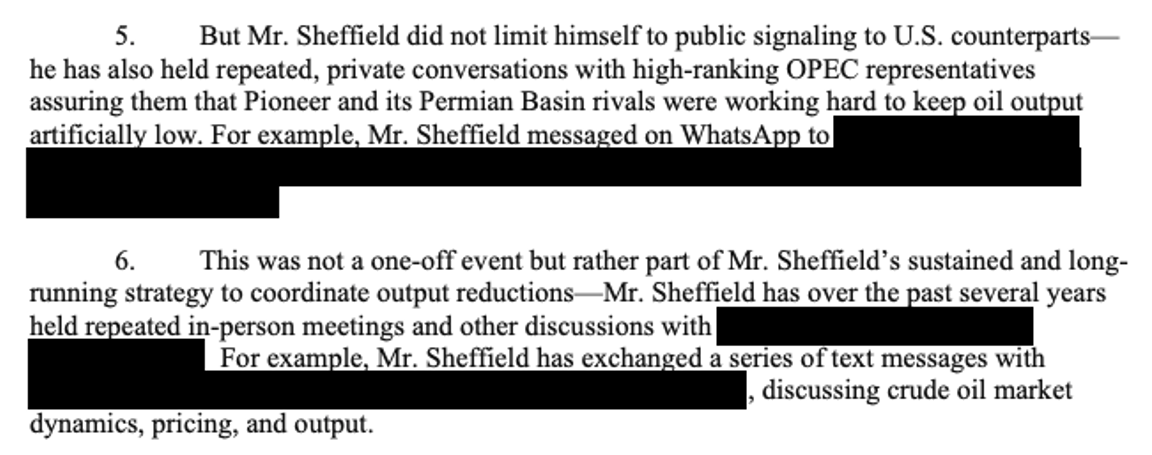

THE SCOOP The Federal Trade Commission plans to recommend a potentially criminal case against the former CEO of Pioneer Natural Resources for comments he made to Texas rivals suggesting they coordinate ways to drill less oil, people familiar with the matter said. The FTC yesterday barred Scott Sheffield, who led Pioneer until the end of 2023 and orchestrated its pending merger with Exxon, from sitting on the combined company’s board as a condition of approving the deal. The agency doesn’t have criminal authority but is looking to refer the matter to the US Justice Department, the people said. In text messages obtained by the government, Sheffield discussed ways to curtail production and assured officials at OPEC+, the cartel of oil-producing countries that includes Saudi Arabia, Russia, and Venezuela, that Pioneer and its Texas rivals were trying to keep oil output artificially low. “If Texas leads the way, maybe we can get OPEC to cut production,” Sheffield wrote, according to the government’s redacted complaint. “Maybe Saudi and Russia will follow. That was our plan,” he said, adding: “I was using the tactics of OPEC+ to get a bigger OPEC+ done.” The government’s complaint “reflects a fundamental misunderstanding of the US and global oil markets and misreads the nature and intent of Mr. Sheffield’s actions,” a spokesman for Pioneer said. “Mr. Sheffield focused on legitimate topics such as investor feedback on independent oil and gas company growth and capital reinvestment frameworks [and] unfair foreign practices that threatened to undermine US energy security.” The FTC expanded its criminal referral program in 2021 and has worked closely with federal prosecutors on a case against Reckitt Benckiser, for thwarting generic competitors to its opioid-addiction treatment Suboxone. “At a time when major corporate lawbreakers can treat civil fines as a cost of doing business, government authorities must ensure that criminal conduct is followed by criminal punishment,” FTC Chair Lina Khan, who has made the issue a priority, said at the time. LIZ’S VIEW Shale producers competed themselves into financial ruin in the 2010s, spending billions of dollars to drill new wells and acquire acreage. Nobody is eager to do that again, and “capital discipline” has become the industry’s watchword. That’s why Exxon is buying Pioneer — and why Chevron is buying Hess, Diamondback is buying Endeavor, and Occidental is buying CrownRock, all since last September. “All the shareholders that I’ve talked to said that if anybody goes back to growth, they will punish those companies,” Sheffield said in 2021, when Pioneer announced it would cap its annual production increase at 5%. A Pioneer spokesman said today that Sheffield’s conversations with big investors, including major pension funds, starting in 2019 set him on this belt-tightening path. The problem isn’t saying those things on earnings calls and in media interviews. It’s saying them to competitors and OPEC officials on WhatsApp, as the government alleges Sheffield did.  What looks like capital discipline to a CEO who doesn’t want to get yelled at by his shareholders can easily look like collusive behavior to prosecutors. As a merger fix, though, this is pretty strange. As the FTC’s two dissenting commissioners wrote, Sheffield’s past actions have little bearing on Exxon’s future ones, and anyway Pioneer is the disappearing company here. “We fear instead that the Commission is leveraging its merger enforcement authority to extract a consent from Exxon rather than addressing the conduct of one misbehaving executive,” the two commissioners wrote. But Khan has expanded the FTC’s non-merger enforcement efforts, moving to ban non-competes and give more protections to gig workers. Merger approval is a powerful tool to punish other, unrelated behavior that the government doesn’t like. For example, the Justice Department in 2022 cleared the merger of two chicken-processing companies in exchange for the companies agreeing to an $85 million settlement for suppressing workers’ wages. One final thought: The FTC has been aggressively swatting down deals, and to the extent this approval bodes well for similar deals like Chevron-Hess, I’m surprised to see it allow a generational consolidation in Big Oil in an election year. Countervailing pressures around energy independence and national security seem to have trumped pocketbook concerns. |