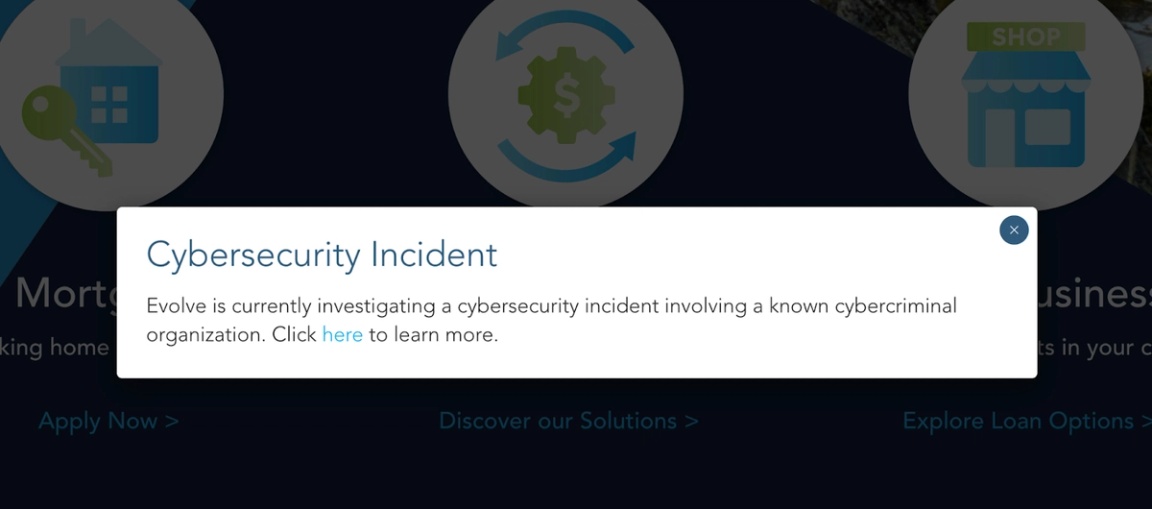

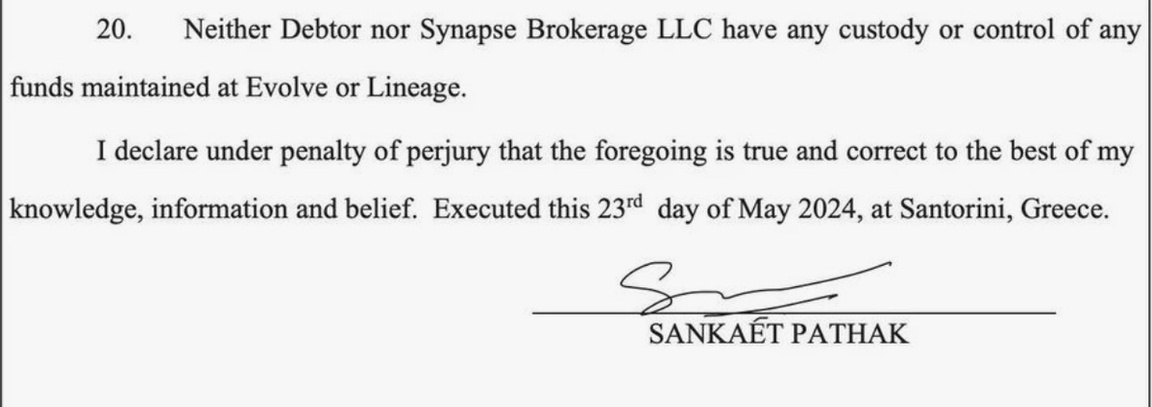

THE NEWS Relationships between fintech apps and the banks to which they offload the nettlesome work of safeguarding customers’ money need closer scrutiny, the top US consumer-finance regulator told Semafor. “There is a ‘move fast and break things’ mentality” in a fintech industry that generally emphasizes the tech over the fin, said Rohit Chopra, director of the Consumer Financial Protection Bureau. “In some circumstances, that’s OK. In other circumstances … it’s just catastrophic.” The catastrophe Chopra was talking about, at a Semafor event Wednesday in Washington, is the recent collapse of a software company that played an invisible but crucial role in the booming world of financial apps. Startups with names like Yotta, Hopscotch, and Dwolla have exploded over the past decade, funded by venture capital and promising to make banking easier, faster, and even fun. They offer banking products like deposit accounts and paycheck advances, but aren’t banks themselves. Instead, they send customers’ money to small banks that actually hold the cash. Sitting in the middle is — was — Synapse Financial, keeping track of whose money was where. When Synapse filed for bankruptcy in April, it shut off a critical system, freezing hundreds of millions of dollars in deposits. Courtroom finger-pointing has done little to clear up the situation. Synapse says its partner bank, a small Arkansas lender called Evolve, owes its customers $50 million. Evolve has questioned the accuracy of Synapse’s ledgers. Customers — most of whom have never heard of either company — are left hanging. Chopra said the CFPB has “long had an issue with rent-a-bank” models. He declined to say whether the agency was investigating Synapse’s collapse, but called it an “obvious and serious lapse of judgment.”  Tierney Cross/Semafor Tierney Cross/SemaforLIZ’S VIEW What happened at Synapse is a feature, not a bug, of this system. That makes it a tough problem for regulators like Chopra: Bugs can be fixed, but stamping out features kills the entire business model. Yotta, the app that’s been most caught up in the mess, is basically an online lottery. But like other companies, ranging from Starbucks to Venmo, it knows that one way to keep users coming back is to have them put money into a digital wallet. Thus: YottaCash. (“You can play YottaCash in any games including Moonshot and Mines where you have the chance to win more YottaCash,” the company’s FAQ page explains.) But Yotta isn’t a bank — venture capital firms don’t invest in banks; they invest in addictive apps — and so it needs someone else to hold that cash. Giants like JPMorgan can’t be bothered. So the money ends up at small banks like Evolve that don’t have big compliance and vendor-management budgets. They have few branches, and have made an entire business model of providing white-labeled accounts for fintech firms. And its pathway to those banks is Synapse, which bills itself as “the largest banking as a service platform” (“X as a service” is the 2020s version of “Uber but for…” the great scourge of the 2010s startup scene.) Its online pitch asks “Is it possible to launch deposit or credit products in a matter of weeks?” Maybe it shouldn’t be! Evolve may end up in the clear here, but this is a bank whose website today greets visitors with this:  Synapse, too, may ultimately be blameless of anything more than a messy bankruptcy. But its contract with one of its biggest partners seemingly allowed it to shut off systems with little notice. Its CEO signed off on the company’s bankruptcy filing from Santorini, which doesn’t inspire a ton of confidence.  FDIC board member Jonathan McKernan told my colleague Gina Chon at yesterday’s event that this combination of scrappy banks and growth-hungry tech companies is concerning. He said the agency — which fired its own warning shot to fintech-bank partnerships last year when it dinged a popular app partner, Cross River Bank, for its lending practices — should consider “some black and white rules of the road.” “It’s not enough for a bank to have in their contract a provision that says the partner is going to perform actions X, Y, and Z,” McKernan said. “The bank has to actually monitor that the partner is performing steps X, Y, and Z, and then they have to have the risk management expertise within the bank to kind of think more globally, big picture …. And that doesn’t happen a lot, candidly.” I think we’ll see more fintech companies opt out of this system and become banks themselves — either by buying one, as Lending Club and SoFi have done, or applying for their own charters like Varo did. Robinhood CEO Vlad Tenev hinted that that’s in the cards when we spoke in February. “Certainly we’re not ideologically opposed,” he said. “As we get more and more into lending, obviously, the calculus behind the business changes.” It’s not easy (regulators are skeptical) or cheap (Varo’s CEO told Banking Dive that the process cost $100 million and took three years) but it nixes the risks that come from relying on unreliable partners. Plaid President Jen Taylor's view on trust between consumers and fintech. → |

|