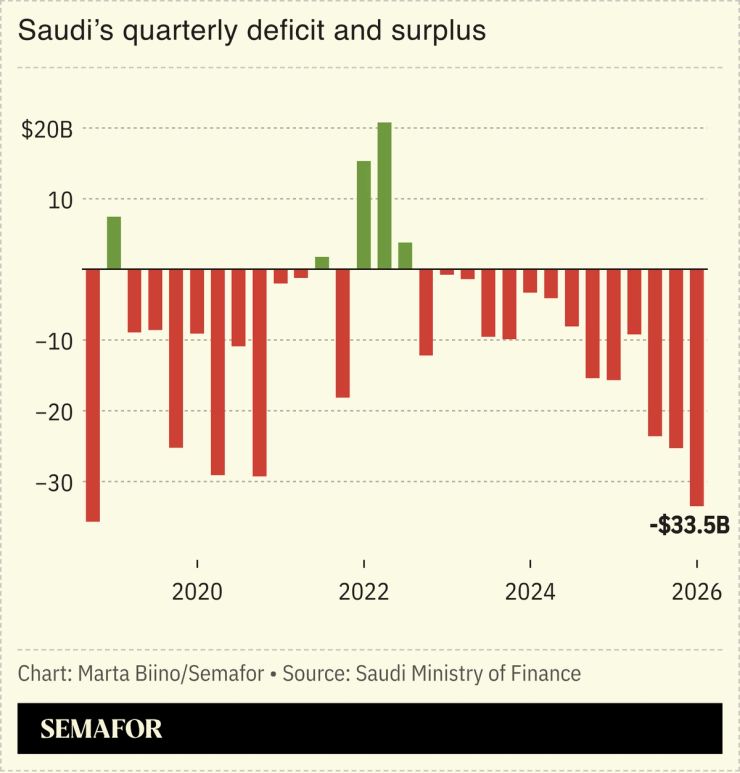

Saudi Arabia recorded its biggest quarterly deficit since 2018 as the kingdom ramped up spending to offset the effects of the Iran war and a slowing domestic economy. Spending on new projects surged by more than 50% compared to a year earlier, with military and transport outlays also up significantly.

The kingdom has managed to divert most of its oil exports to ports on the west coast, helping to shore up declining government revenues. It has also taken steps to bolster its role as a logistics hub for the wider Gulf region, and support the flow of goods disrupted by the closure of the Strait of Hormuz.

Debt rose by the most in years as the government leaned on Saudi private lenders and didn’t touch its stock of foreign reserves. Most of the year’s financing needs were raised before the Iran war, but if the country needs to raise more it will likely continue to rely on local markets and private deals, the National Debt Management Office said.

Overall economic growth in the kingdom slowed in the first quarter. However, Saudi Arabia’s oil revenues are thought to be up by about 10% as a result of higher prices, outweighing the impact of the strait’s closure, according to Goldman Sachs.

Economists say the government may have been front-loading spending to support growth while the Public Investment Fund has been cancelling some contracts, and investing in preparation for hosting the Hajj pilgrimage in late May.

Tim Callen, the former IMF mission chief to Saudi Arabia, told Asharq Business that the increase in capital expenditure in the first quarter was notable because the kingdom rarely deploys that much spending so early in the year. He said he expects military spending to rise throughout the year, and that oil revenues may also get a boost, as higher prices will likely be more fully reflected in the next quarter because of the lag between crude exports and payments.