The News

Fossil fuels are ending 2023 with a bang.

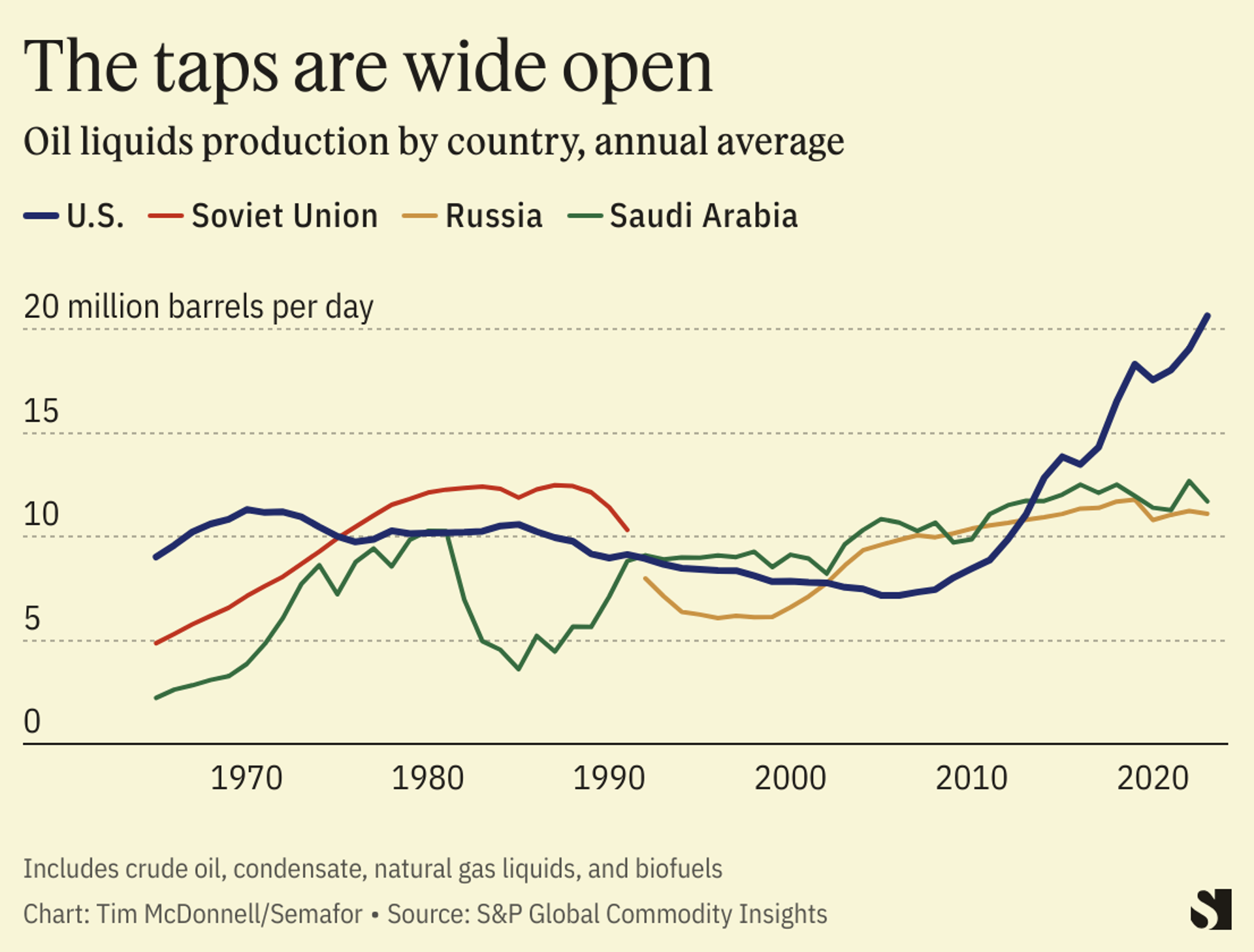

On Wednesday, one week after world governments agreed at COP28 to “transition away from fossil fuels,” oil companies including Shell and Hess bid a collective $382 million for drilling rights in the Gulf of Mexico, the most for an auction there since 2015. The auction closely followed the release of data showing that U.S. oil production is now higher than in any country at any time in history, reaching about 13.3 million barrels per day in the fourth quarter.

In this article:

Tim’s view

The dissonance between the political agreement at COP28 and the reality of the current oil market underscores the contradictory phase of the energy transition the global economy went through in 2023. The end of fossil fuels is on the horizon, but in the meantime global demand for oil and gas is rising and companies are responding accordingly. And yet, 2023 was also a banner year for renewables.

The pace of global decarbonization is set by the tension between market signals favoring fossil fuels and those favoring clean energy, and in 2023 those signals clashed more directly than ever before.

There are a few other key data points from the past year that signal where the balancing act between old and new forms of energy is headed in the year ahead:

Investment globally in clean energy for every dollar invested in fossil fuels this year. Five years ago, the ratio was one-to-one. In 2023, for the first time, global investment in solar topped investment in oil production. This shift shows that government subsidies and tax credits to draw clean energy investment are working, and that oil companies are being cautious about making big new investments in exploration and production.

Production cost per watt for solar power cells made in China this year, 42% lower than in the previous year. The investment ratio above is even more impressive in light of the plummeting cost of clean energy, which allows every dollar invested to yield a lot more clean electrons.

Share of capital spending by global oil and gas companies on energy transition technologies, including renewables and carbon capture. This is up from less than 0.5% a few years ago. But it shows that oil companies are still struggling to decide where they fit in the transition. They have a lot of technical expertise and manpower to leverage on changing the energy system, but as long as this capex figure remains pitifully low it’s clear that oil executives think their shareholders would prefer for them to stick to their traditional business.

Metric tons per year of liquified natural gas export-terminal capacity under development worldwide. That’s 18% more than in the previous year, and comes largely in response to Europe’s frantic efforts to replace Russian pipeline gas and efforts by Asian countries to replace coal in their electric grids. The global growth in renewables isn’t happening fast enough to prevent some major long-term investments in fossil fuel infrastructure from moving forward, or to quell deep-seated insecurities that many policymakers and industry leaders have about energy stability. (There’s a risk that some of this LNG infrastructure will wind up “stranded,” made redundant before its multi-decade amortization period is up.)

Average wait time for utility-scale electricity projects to connect to the grid in the United States. The “interconnection queue” is at least two years longer than it was in the mid-2010s, and remains the number-one obstacle to bringing more renewables online. This is a problem that can only be fixed with new laws and policies, not by the market alone.

Barrels of oil per day displaced globally by EVs last year. That’s still a tiny slice of the 100 million barrels of oil consumed daily across the global economy. But if the speed at which the economy can “transition away” from fossil fuels is mainly a function of how quickly demand for them dissipates, EV adoption is the factor making the biggest near-term impact on oil. Peak demand for oil for road transportation will likely arrive by 2027, BloombergNEF projects. EV sales are a critical metric to watch in the year ahead.

Drop in venture capital investment in climate tech in 2023 compared to the previous year. That figure isn’t quite as bad as it seems: Overall VC funding fell even more, by 50%. In the year ahead it will be important to watch whether this figure can bounce back, and even more importantly whether a greater share of climate tech investment can shift from seed-stage startups to the commercialization of more mature cutting-edge technologies, which remain often stuck in a “valley of death.”

Number of billion-dollar disasters to hit the U.S. in 2023, a record. This figure isn’t related to the energy market per se, but shows the urgency of the climate crisis, which was a key factor behind the COP28 fossil fuel agreement.

Know More

Record-breaking U.S. oil production isn’t just a response to demand, or a matter of companies trying to chase higher crude oil prices as their rivals in OPEC countries continue to cut their production quotas. It’s more the result of the wave of consolidation that has swept through the U.S. shale patch in the last year, like ExxonMobil’s $60 billion acquisition of Pioneer Natural Resources. The larger companies have more engineering resources to squeeze the most oil out of the assets they’ve acquired, per dollar of operating expenses. So production is increasing even though the total number of active drilling rigs in the U.S. is currently 15% below the 2022 average.

The View From China

China’s greenhouse gas emissions hit a record in 2023, passing 4 billion metric tons for the first time. But they could be set to begin a structural decline within the next couple of years even as more coal power comes online, as the rate of new renewable energy additions comes close to exceeding the rate of electricity demand growth.